Get actionable data before loss occurs with the Default Timeline Manager

More than ever, FHA mortgage servicers are experiencing reduced financial recoveries from avoidable errors that occur prior to the claims process. These delays occur throughout the default lifecycle – from early delinquency all the way to the foreclosure process – in the form of missed compliance milestones which could be from untimely oversight, inaccurate data, incorrect processes and automation or any combination of the three.

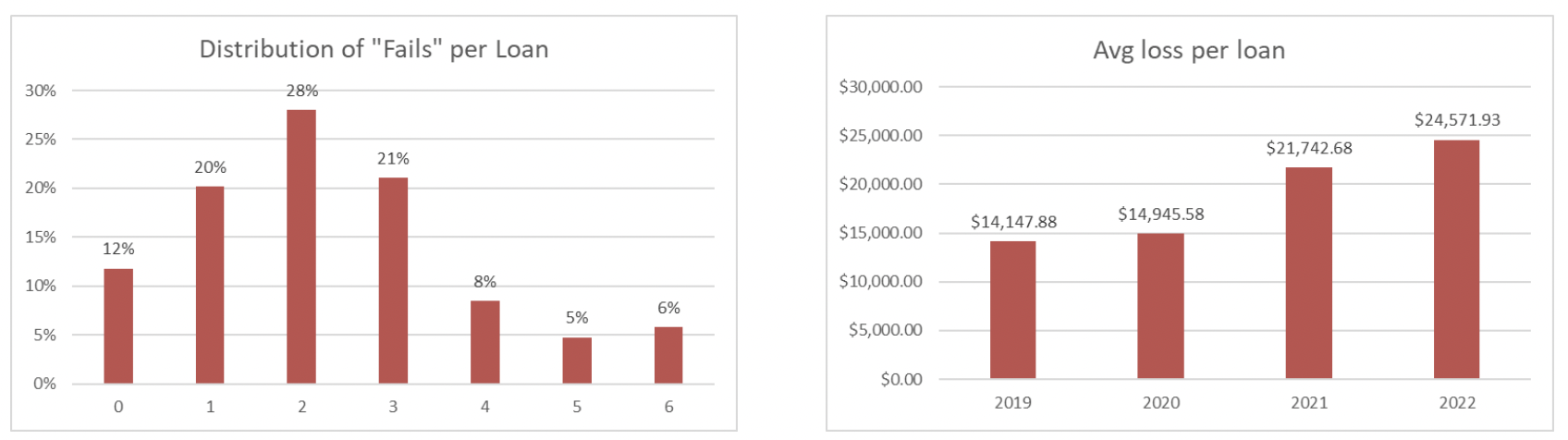

* Based on an internal, multi-year review of over 7,500 claims from CRFS servicing base.

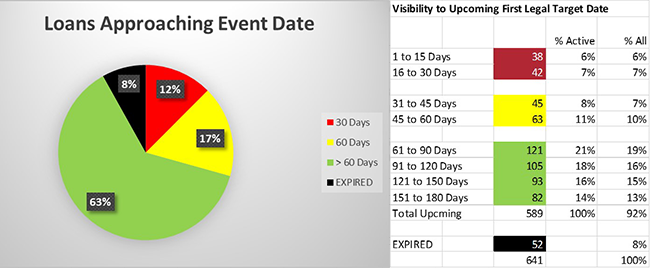

Example of Reporting Output for the First Legal Deadline metric